I remember hearing a story several years ago from one of my colleagues about an AR fraud that was discovered by an auditor while performing an inventory roll forward. The person telling this story was and remains well known in the Asset Based Lending arena, so needless to say I was quite intrigued about how a fraud that occurred with AR could be found while performing an inventory review. I’ll try to retell the story here; hopefully, my memory will do it justice. In addition, I’ll try to relate the procedures performed by the auditor to examination procedures performed today.

About the Fraud

The Company being audited sold to large retail chains and stores with JC Penney being by far the largest customer. Deliveries were made by company trucks. Most ordering and invoicing was done via “EDI.” Because of these processes and the customer base, third party documentation to support sales were not readily available. I don’t recall if phone verifications were performed by the lender or not but if they were it would be feasible that due to the customer base (large retailers with JC Penney as a large concentration) they were often left open or unresolved or were of a small sample in relation to total AR. Anyone that is familiar with JC Penney’s billing requirements knows that it requires a separate invoice for each location. This results in a very large number of invoices often for small dollar amounts.

The Company being audited was on a periodic inventory system. Inventory was assigned to the lender based on monthly physicals. Because of this, one of the procedures that the lender required was the completion of an inventory roll forward. The process involved taking the inventory per the last full physical, adding purchases and other direct costs, then subtracting the cost of goods sold to arrive at ending inventory. Certainly nothing special there, it seems like a fairly simple procedure and if you can add and subtract it should be easily accomplished.

The problem (and in retrospect the opportunity for finding the fraud) was in how to get the cost of sales number. Because the company was on a periodic system, the cost of sales was not readily available. The examiner did have the beginning inventory number, the purchases and other costs incurred were also readily available. Although the actual cost of sales were not available, the auditor did have sales and credits from the AR roll forward. He also had the FYE financial statements.

As a substitute for the actual cost of sales the auditor used the sales per the AR roll forward. The cost of sales was determined by multiplying net sales (gross sales per the roll forward less dilutive credits) by the reciprocal of the gross profit % (i.e. 100% less the GP%). The gross profit percentage was easily derived from the financial statements. After performing the simple math involved to get to the cost of sales and then the ending inventory, the roll forward resulted in negative inventory!.

Just for illustrative purposes lets assume the following:

- The audit occurred 11 months after the last full physical

- Inventory turnover is approximately 8 times per year or 45 days.

- Per the inventory assignments made to the lender, the inventory level had little variation with no seasonality present.

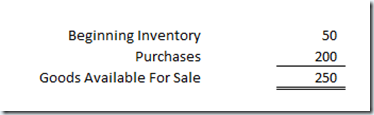

- Beginning inventory, purchases and the resulting goods available for sale were as follows:

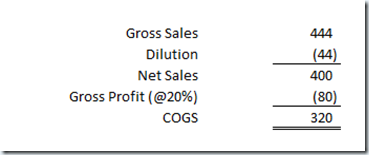

- The calculation of Cost of Sales was based on sales of $444M, credits of $44M (dilution was 10%), and a 20% gross profit percentage from the year end financial statements:

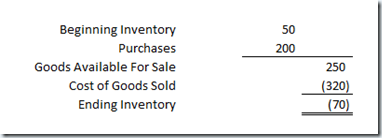

- The inventory roll forward results in a negative $20M inventory amount as follows:

After calculating the negative inventory the examiner was certain that something must be wrong with is process or assumptions, so he/she went back and verified all of the numbers used, naturally every thing thing checked out. After verifying and re-verifying the amounts used he/she was at his wits end and was certain that something in his process or assumptions were wrong. The examiner sheepishly approached the senior auditor and explained the dilemma, noting that something must be wrong as it was impossible to have negative inventory!

After the reviewing the results and the assumptions the senior examiner along with the audit manager started to put two and two together. They noted that the AR test results were far from exemplary due to the delivery and ordering systems. In addition, AR verifications were at best inconclusive as only a small % of the AR could be verified if a response was actually received. After reviewing the results of the exam with the account manager, the company was approached and a request was made to speak with the buyer at JC Penney directly. This would allow the lender to verify that the shipments to JC Penney were indeed in line with the orders made by the buyer. After providing several wrong numbers and/or names of the JC Penney buyers the Company realizing that if could not put off the lender indefinitely finally admitted that the sales to JC Penney were overstated. They were based on future orders that were scheduled for delivery but not yet made.

Some Things to Consider for Inventory Roll Forwards

- Often when performing inventory roll forwards the emphasis is on getting as close to the ending inventory balance as possible. I think that the above points out that this may not be the best mind set. Its more important to understand the relationships of the various roll forward components and ensuring that those components are accurately reflected. If that is done the ending balance that is derived should be trusted and if different than the reported inventory amount then that difference should be explained rather than discounted.

- None of the various components of the roll forward should be plugged. There must be some rationale for the amounts used. The example above points out how important this is. It would have been very easy for the examiner to simply “plug” the COGS to arrive at the ending inventory. The discrepancies between the sales per the AR roll forward and the inventory roll forward could have been easily overlooked had this been done.

- Similarly, when performing inventory roll forwards the emphasis is also on calculating the inventory turnover statistic. Although this is an important tool for measuring how a company is managing its inventory, and is certainly worthy of the effort spent to get it, it should not be the sole reason for completing the roll forward. Other items of note can and should include:

- Comparison of cost of sales per the inventory roll forward to the sales per the AR roll forward.

- After adjusting for the GP% do the sales per the two procedures (AR and Inventory roll forwards) agree or are they at least within a certain tolerance level? If not why?

- Are the GP%’s noted consistent with the reported GP%? Are there material differences? if so why?

- Are the components of the cost of sales used in the roll forward consistent with the cost components of the inventory? Are the material, labor and other direct costs consistent with the inventory component costs? If not why not?

- Comparison of cost of sales per the inventory roll forward to the sales per the AR roll forward.

Conclusion

Hopefully, the above points out that the inventory roll forward is often an overlooked tool that can be used to gain insight into several areas of a company’s business or collateral that are in addition to its inventory management capabilities. The roll forward can be used to:

- Indirectly verify the sales reported

- Verify the gross profit reported

- Verify the various cost components of the inventory,

That’s it for now. Please feel free to leave a comment or question. If you would rather contact me directly you can email us at [email protected]

For samples of reports prepared by ECG please visit http://www.ecgenterprises.com/Reports